15 Things Learned:

1. Anyone who is not classified as either employed or unemployed is not in the labor force.

2. The Census Bureau conducts a monthly study called the current population survey.

3. Full employment means about 95% of the population is employed.

4. Seasonal unemployment effects mainly agricultural workers.

5. Unemployment rate is the most closely watched and highly publicized labor force statistic.

6. An increase in the average price level of all products in an economy is called inflation.

7. A decrease in the average price level of all goods and services in an economy is known as deflation.

8. To measure the price level, economists construct a price index.

9. The worst degree of inflation is called hyperinflation.

10. High interest rates lead to less consumer spending.

11. Aggregate supply is the total amount of goods and services produced throughout the economy.

12. The poverty threshhold is the lowest income level that a family needs to maintain a basic standard of living.

13. Poverty thresholds are adjusted annually based on changes in the consumer price index.

14. The data used to plot a Lorenz Curve can also be used to compute the Gini Index.

15. One suggestion for improving income equality is raising the minimum wage.

Monday, January 24, 2011

Wednesday, January 19, 2011

Vocab Terms List (Blog 21)

National Income Accounting-refers to the bookkeeping system that a national government uses to measure the level of the country's economic activity in a given time period.

Gross Domestic Product-The monetary value of all the finished goods and services produced within a country's borders in a specific time period, though GDP is usually calculated on an annual basis.

Output-Expenditure Model-Gross Investment, Personal Consumption expenditures, government purchases of goods and services, and net exports of goods and services, or exports minus imports(X-M)/(C+I+G+(X-M)=GDP

Personal Consumption Expenditure-Consumer Purchases

Gross Investment-the total amount of investment without taking account of the cost of depreciation

Nominal GDP-A gross domestic product (GDP) figure that has not been adjusted for inflation.

Real GDP-An inflation-adjusted measure that reflects the value of all goods and services produced in a given year, expressed in base-year prices.

Price Index-Index that tracks inflation by measuring price changes

Underground Economy-consists of all trade that occurs without government permission or effectual intervention

Gross National Product-GNP is the total value of all final goods and services produced within a nation in a particular year, plus income earned by its citizens minus income of non-residents located in that country.

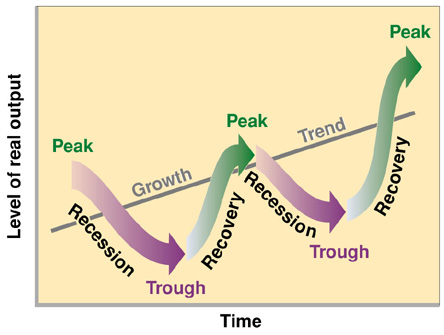

Business Cycle-The recurring and fluctuating levels of economic activity that an economy experiences over a long period of time.

Expansion-Period of Economic Growth

Peak-Point at which economy is at its strongest and most prosperous.

Contraction-Recession

Depression-Prolonged and severe recessions

Trough-Demand, Production, and employment reach their lowest levels.

Leading Indicators-An economic indicator that changes before the economy has changed.

Coincident Indicators-An economic indicator which varies directly with, and at the same time as, the related economic trend, thereby providing information about the current state of the economy.

Lagging Indicators-A measurable economic factor that changes after the economy has already begun to follow a particular pattern or trend.

Real GDP Per Capita-GDP), gross national product (GNP) and net national income (NNI), all are indicators of a country's economic power. Many scholars and critics argue that economic components that are included in calculating GDP per capita are unscientific and lack various critical aspects of the economy. Nevertheless, in almost all countries, GDP per capita is used as a benchmark for measuring nation's economic progress.

Labor Productivity-A measurement of economic growth of a country. Labor productivity measures the amount of goods and services produced by one hour of labor.

Productivity Growth-in economics, the output of any aspect of production per unit of input. It is a measure of the output of a worker, machine, or an entire national economy in the creation of goods and services to produce wealth.

Capital-To-Labor Ratio-The ratio of capital available per worker

Capital Deepening- Capital deepening is an increase in capital intensity.

Gross Domestic Product-The monetary value of all the finished goods and services produced within a country's borders in a specific time period, though GDP is usually calculated on an annual basis.

Output-Expenditure Model-Gross Investment, Personal Consumption expenditures, government purchases of goods and services, and net exports of goods and services, or exports minus imports(X-M)/(C+I+G+(X-M)=GDP

Personal Consumption Expenditure-Consumer Purchases

Gross Investment-the total amount of investment without taking account of the cost of depreciation

Nominal GDP-A gross domestic product (GDP) figure that has not been adjusted for inflation.

Real GDP-An inflation-adjusted measure that reflects the value of all goods and services produced in a given year, expressed in base-year prices.

Price Index-Index that tracks inflation by measuring price changes

Underground Economy-consists of all trade that occurs without government permission or effectual intervention

Gross National Product-GNP is the total value of all final goods and services produced within a nation in a particular year, plus income earned by its citizens minus income of non-residents located in that country.

Business Cycle-The recurring and fluctuating levels of economic activity that an economy experiences over a long period of time.

Expansion-Period of Economic Growth

Peak-Point at which economy is at its strongest and most prosperous.

Contraction-Recession

Depression-Prolonged and severe recessions

Trough-Demand, Production, and employment reach their lowest levels.

Leading Indicators-An economic indicator that changes before the economy has changed.

Coincident Indicators-An economic indicator which varies directly with, and at the same time as, the related economic trend, thereby providing information about the current state of the economy.

Lagging Indicators-A measurable economic factor that changes after the economy has already begun to follow a particular pattern or trend.

Real GDP Per Capita-GDP), gross national product (GNP) and net national income (NNI), all are indicators of a country's economic power. Many scholars and critics argue that economic components that are included in calculating GDP per capita are unscientific and lack various critical aspects of the economy. Nevertheless, in almost all countries, GDP per capita is used as a benchmark for measuring nation's economic progress.

Labor Productivity-A measurement of economic growth of a country. Labor productivity measures the amount of goods and services produced by one hour of labor.

Productivity Growth-in economics, the output of any aspect of production per unit of input. It is a measure of the output of a worker, machine, or an entire national economy in the creation of goods and services to produce wealth.

Capital-To-Labor Ratio-The ratio of capital available per worker

Capital Deepening- Capital deepening is an increase in capital intensity.

Tuesday, January 11, 2011

Coincident/Lagging Indicators

Coincident Indicators List

(i) Number of employees on non -agricultural payrolls (in Total unemployment Rate

(iii) Gross National Product in constant price (iv) Index of Industrial Production

(v) Personal Income (in money terms)

(vi) Manufacturing and trade sales (in money terms)

(vii) Sales of retail stores (in money terms)

Lagging Indicators

1. The value of outstanding commercial and industrial loans

2. The change in the Consumer Price Index for services from the previous month

3. The change in labor cost per unit of labor output

4. The ratio of manufacturing and trade inventories to sales made

5. The ratio of consumer credit outstanding to personal income

6. The average prime rate charged by banks

7. The inverted average length of employment

I believe these two list tell a lot about the economy and the market. They describe how to understand and read the marketplace so that you can make smart and wise investments and decisions and not lose money whether you are a business or a person.

(i) Number of employees on non -agricultural payrolls (in Total unemployment Rate

(iii) Gross National Product in constant price (iv) Index of Industrial Production

(v) Personal Income (in money terms)

(vi) Manufacturing and trade sales (in money terms)

(vii) Sales of retail stores (in money terms)

Lagging Indicators

1. The value of outstanding commercial and industrial loans

2. The change in the Consumer Price Index for services from the previous month

3. The change in labor cost per unit of labor output

4. The ratio of manufacturing and trade inventories to sales made

5. The ratio of consumer credit outstanding to personal income

6. The average prime rate charged by banks

7. The inverted average length of employment

I believe these two list tell a lot about the economy and the market. They describe how to understand and read the marketplace so that you can make smart and wise investments and decisions and not lose money whether you are a business or a person.

Thermometer

-The top triangle of the pyramid Is the C+ in the GDP formula and it represents Personal Consumption Expenditures.

-The top triangle of the pyramid Is the C+ in the GDP formula and it represents Personal Consumption Expenditures. -The portion of the pyramid directly under that represents the I+ in the GDP formula and it represents the Gross Investment portion.

-The portion of the pyramid directly under that section is the G+ in the GDP formula which has to do witht the government purchases of goods and services.

-The portion of the pyramid under that section is the (X-M)= in the GDP formula which is the Net Exports of goods and services, and the Net Imports of goods and Services.

-Put all of those together and they create GDP (Gross Domestic Product).

Thursday, January 6, 2011

Videos and Link

After watching the two videos that center around the premise of the business cycle, i found that both videos were more silly than helpful in my opinion, they were fun, and creative, but to childish if you ask me. I would have picked a different way of going about teaching the subject. I believe the qwiki source is a better way to learn the topic, because it is more focused and still has a sense of humor to it that you can enjoy.

http://www.12manage.com/description_business_cycle.html

http://www.12manage.com/description_business_cycle.html

Tuesday, January 4, 2011

Business Cycle Theories

1. Graph number one is good because it depicts recession and growth are in the business cycle and it also shows you what there potential to become is if everything was perfect. So it gives a real life view as well as an artifiicial one.

2. Graph number two is an alright representation because it is sort of confusing in a sense because it does not tell you how the different parts relate to eachother, but it does tell you part of the cycle itself.

3. Graph number three is a mix of both one and two and does do a good job of representing its purpose of describing the business cycle. It shows the process that the business cycle continuously goes through on a daily basis.

-I am presenting the JC-Wiz Award for best Graph to graph number one for its outstanding representation of the business cycle and solid creativity and good looks to the naked eye.

Monday, January 3, 2011

Visual To Help On Chapter Test

I think that this visual aid will be able to help me/us on the chapter test.

Definitions:

Macroeconomics-The study of the overall aspects and workings of a national economy, such as income, output, and the interrelationship among diverse economic sectors.

GDP-Gross Domestic Product. The total market value of all final goods and services produced in a country in a given year, equal to total consumer, investment and government spending, plus the value of exports, minus the value of imports.

GNP-Gross National Product. GNP is the total value of all final goods and services produced within a nation in a particular year, plus income earned by its citizens (including income of those located abroad), minus income of non-residents located in that country.

Subscribe to:

Posts (Atom)